The market responded well to today's Treasury auction. Bid to cover was 2.26 with a high yield of 3.3% and indirect bidders representing 33%.

As a side note, senior tranches of CMBS (commercial mortgage backed securities) are now back to trading around 800 basis points above swaps due to ratings agencies stating that they will not retain their AAA rating and therefore will not be allowed to participate in the TALF program.

Homebuilders are getting slammed today. Gold is trading strong along with oil. Piggies (banks) are strong and high beta is leading the charge.

Heading into the final hour. Good luck.

Thursday, May 28, 2009

Irony?

I just read that if John F. Kennedy was still alive, he'd turn 92 tomorrow. This was a quote that a reader quickly chimed in with.

“A nation that is afraid to let its people judge the truth and falsehood in an open market is a nation that is afraid of its people.” - J.F.K.

A little food for thought.

“A nation that is afraid to let its people judge the truth and falsehood in an open market is a nation that is afraid of its people.” - J.F.K.

A little food for thought.

Wednesday, May 27, 2009

Dangerous Waters

I'd like to start off by saying that I'm generally a pessimistic person when it comes to today's economy, politics and the overall mindset of the American citizens. So me being bearish on the markets/economy shouldn't be a surprise to anyone. But after the action in the markets today, I really am getting worried about the future prospects of our economy and therefore the standard of living in this country. Practical economists, which there seem to be very few of today, at least in Washington, have been worried for quite a while. The velocity of this pending tidal wave seems to be gaining speed each day, at least in my humble opinion. I remind you, I don't have much hands on experience dealing with the changing of business cycles, shifts in social mood, economic recessions or trading stocks while going through turbulent times. I do consider myself to be a very practical and analytical individual, who puts in a lot of time studying those subjects. What I'm getting at is that I truly believe bad times are coming. When I say bad times, I don't mean a recession for a few years with low GDP growth and high unemployment. I'm thinking more along the lines of a complete change of the way people live within this country.

We have seen the first of many changes beginning with consumer psychology. The bling bling days are over folks. The longer you want to hold on to those days, which were great, don't get me wrong, the more you are ill-preparing yourself for the future. Social moods are shifting towards a more austere lifestyle and there are signs of this all over. Listen to commercials on the radio or on t.v. You'll hear advertising in commercials poking fun at federal bailouts or how everyone needs to save money these days or how in these tough times you should look to the such and such product to help you feel good again. Advertising is all psychology and the advertisers are changing their methods before the consumers, as a whole, have changed their psychology. The marketers are smart and see shift towards a darker social mood, which is why they already have ads to coincide with these shifts. Now, a darker social mood doesn't mean that everyone is going to become gothic, start wearing trench coats and dying their hair black. It simply suggests that as a whole, the people of this country hit a peak on their positive social moods and things are naturally going to be in a rut for some time. It all moves in cycles. It just so happens that this cycle has the potential to be the cycle of all cycles. A mega cycle, if you will. There is a lot on the line here with societal acrimony seemingly deteriorating day by day along with the global economy. I could go on for days about this, but I think you get the picture. The sooner you can prepare for these darker days, the better position you'll be in to profit in those tough times.

As for the market today, I'll keep it quick. The 5-yr Treasury auction actually went well today. Normally this would be a great sign for the market and equities would have rallied, but this couldn't be further from the truth. The odd thing was that foreign demand for the shorter term Treasuries was higher than it has been in past auctions. Combine that with the fact that the rate on the 10-yr jumped to 3.7%...yea that's right 3.7% (now up 46.25% since the Fed announced it purchasing of Treasuries in mid March) and you'll notice that investors are skittish about the longer term debt in the U.S. This led to a major sell off in the long dated Treasuries and forced yields up again. As I've said before, rising 10-yr yields is going to kill any type of housing recovery. Historically, with the 10-yr at 3.7%, 30-yr fixed mortgage rates are around 5.6%. Right now they are at 5.06% and just a month ago they were 4.8%. This means that people won't be able to sell their houses at the prices they are asking now, if mortgage rates continue to rise. This will lead to further housing price declines and therefore make the banks balance sheets even more toxic. It's like a death spiral. The 2 & 10 spread (10-yr treasury - 2-yr treasury) widened to its largest spread ever today. This shows that investors will buy short term treasuries, but are nervous about the long term solvency of our sovereign debt and are demanding higher rates of return for the higher risks they are taking. The chart below depicts this.

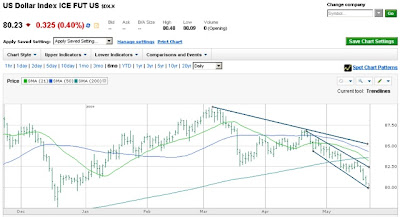

Adding to the fact that Treasuries sold off heavy around 2:30 pm, equities sold off as well. Stocks were trading flat for the most part, but finished down over 2%. This is an ominous sign from where I'm standing. Investors are have no where to hide right now. The dollar has made a small bounce due to technicals, which is a positive sign. We are quickly approaching the point of recognition. The scary thing is that you don't actually know what the point of recognition is, until you are staring the beast in the eyes....and by that time, it's too late to run.

Good luck tomorrow and be careful out there because risks are getting higher each day.

Tuesday, May 26, 2009

Consumer sentiment sends stocks up

The stock market had a great day, posting a 2.63% gain. Futures going into the session were down around 877, which is very close the important support level of 875. This could have led to a big selloff but instead the market moved higher. The main catalyst for the rally was that consumer sentiment came in much higher than expected. Overall, it's a breath of fresh air to hear that consumers are more confident now than in previous surveys. I'm nervous that some of that air may have been contaminated with some nuclear waste, thanks to North Korea. The market rally, economic green shoots and overall improvement in sentiment is going bite people in the ass, WHEN, NOT IF, things turn grim again.

This week is very important because there is over $100 billion in Treasuries being auctioned. Today, $40 billion of 2-yr bills saw a successful auction. Once again this is positive, but a bit irrelevant. Tomorrow and Thursday will be much more telling. Tomorrow $35 billion of 5-yr's are being auctioned and Thursday, $26 billion of 7-yr's. These bonds have a longer maturity and therefore carry more default risk. If these auctions don't go well, things will get ugly quick. The 10-yr note is now trading with a yield around 3.55%. That rate is up nearly 40% since the Fed started its quantitative easing practices on March 17th. I'm going to go out on a limb and say the bond market isn't feeling what the Fed is doing. As I've said before, rates will continue to rise until the government stops spending, plain and simple.

Don't be a sheep and get caught up on the stock market rising. Light volume days like today are very volatile and prices can easily move one way or the other. The bond market trumps the stock market in size and this market should be followed closely. Rates are going up, prices are going down, another deflationary signal. Inflationists have a stronger following, which means I'll take the opposite side and say that deflation will persist much longer than what "most economists" expect. Without going into too much detail, time and price are the ultimate arbiters of our faith, as my friend Toddo would say. Prices are still FAR to high in almost every financial asset and commodity, which means the downward pressure on prices will be around for some time.

Add North Korea to the equation, who is launching nuclear devices for testing, and you have a pretty uneasy global landscape right now. Watch to see how the bond auctions go tomorrow and always follow the dollar, which made its 2009 low on Friday before bouncing back a tiny bit today, due to weakness in Asian currencies caused by North Korea. The storm is brewing folks and you'll want to be prepared for when these waves start crashing down. Good luck tomorrow!

....couldn't help but throw in some comments from the greatest quarterback of this generation.

"What would I do instead of run out in front of 80,000 people and command 52 guys and be around guys I consider brothers and be one of the real gladiators? Why would I ever want to do anything else? It’s so hard to think of anything that would match what I do: Fly to the moon? Jump out of planes? Bungee-jump off cliffs? None of that shit matters to me. I want to play this game I love"

Ahhh almost football season again...thank you Tom Brady.

Thursday, May 21, 2009

Down Goes the Dollar

Something is certainly brewing. On the news front to we had initial clams rise and last weeks reading was revised upward. Upward revisions of economic data seems to be happening very often lately. It gives me the feeling the government is using sneaky maneuvers to try and spur the market short term. When this becomes a trend investors will lose confidence in those figures and more uncertainty will be on the table, which is never good for the market....just a little something to look out for.

Today, the market slipped 1.68%, which was led to one of the best indicators i've found, the Dow Transportations. It has been a lead indicator in recent market drops. It fell almost 4% and was approaching a very critical trendline around 2950. If it is to break through that trendline, we could very well see the market take a bit of a nosedive. With the market unsuccessfully able to break through its 200 moving average twice, I think is a tell. Bank of America, which has been a great tell the past couple of weeks, was off 0.7% and has been acting weird since its stock offering on Tuesday. Basic materials, which have been on a tear, saw a big pullback as well. It's an odd weekend because many investors are away due to Memorial Day and volume has been a bit low.

Home builders were down about 2%. There still will be no recovery in housing for some time to come. Low mortgage rates don't sell houses, low prices do. Tuesday, the Housing starts figure was 12% below consensus. The market reacted negatively to it off the bat, but digested the news and realized it was actually a good sign. Housing starts should fall, we're already sitting on a gluttony of inventory. There is no need for further building. We are still a long way from the bottom of housing because jobs continue to be shed, prices of our necessities are rising, and most people these days don't have enough actual savings to put a down payment on a home.

Anyways, if you really believe that housing is close to a bottom....then explain this chart to me. Yea...scary.

I continue to believe we are near a pretty big move downward. There has been a number of indicators starting to flicker, sentiment that continues to grow negative and news which shows no signs of recovery. Be careful with your investments at this point. The dollar continues to slide which makes those losses even more of an impact. It's time to start looking to move some dollars into foreign currencies.

Treasury prices continue to rise in wake of this week's Treasury buying binge at the Fed. I believe they bought around $14.2 billion in bond's this week, yet interest rates continue to rise. This is the market calling out Treasury Secretary Geithner, who earlier this morning said his job was to sustain a strong dollar. If he is supportive of a strong dollar he will let interest rates rise and have no choice but to stop spending so much money. The U.S. cannot afford to continue to keep buying if rates keep rising. The market wants them to STOP buying because it's killing the dollar.

The dollar has dropped 10% since the market rally around March 9th. Dollar devaluation leads to anything priced in dollars to rise. The market has risen, basic materials has risen, commodities have risen, oil is above $60 and gold is above $950. The dollar droppage has led to a rise in the price of our necessities. That'll will correlate into the prices of companies that deal with those necessities to raise. As if said before, the worst thing that can happen to the U.S., economically, is for the dollar to lose its value.

Today, the market slipped 1.68%, which was led to one of the best indicators i've found, the Dow Transportations. It has been a lead indicator in recent market drops. It fell almost 4% and was approaching a very critical trendline around 2950. If it is to break through that trendline, we could very well see the market take a bit of a nosedive. With the market unsuccessfully able to break through its 200 moving average twice, I think is a tell. Bank of America, which has been a great tell the past couple of weeks, was off 0.7% and has been acting weird since its stock offering on Tuesday. Basic materials, which have been on a tear, saw a big pullback as well. It's an odd weekend because many investors are away due to Memorial Day and volume has been a bit low.

Home builders were down about 2%. There still will be no recovery in housing for some time to come. Low mortgage rates don't sell houses, low prices do. Tuesday, the Housing starts figure was 12% below consensus. The market reacted negatively to it off the bat, but digested the news and realized it was actually a good sign. Housing starts should fall, we're already sitting on a gluttony of inventory. There is no need for further building. We are still a long way from the bottom of housing because jobs continue to be shed, prices of our necessities are rising, and most people these days don't have enough actual savings to put a down payment on a home.

Anyways, if you really believe that housing is close to a bottom....then explain this chart to me. Yea...scary.

I continue to believe we are near a pretty big move downward. There has been a number of indicators starting to flicker, sentiment that continues to grow negative and news which shows no signs of recovery. Be careful with your investments at this point. The dollar continues to slide which makes those losses even more of an impact. It's time to start looking to move some dollars into foreign currencies.

Monday, May 18, 2009

After a relaxing vacation last week, it's back to the craziness of the capital markets on this Monday. I got to spend some time away from work, away from the markets, and paid a visit to my uncle. After about a hundred holes of golf, a number of laughs and a few cold beers, I'm greatful to be surrounded by such a great family. It's important in times like this to get away from the hustle and bustle of our everyday lives and spend some time to reflect with the ones we care about.

Both the Celtics and Bruins have had their seasons ended. They both had great seasons but it's tough to watch your teams go down. The B's somewhat overachieved this year, but showed a lot of heart coming back from 3-1 to force a game 7 and push that game into overtime. I heard Tom Carron on WEEI today say that this years Bruins is similar to the 2003 Red Sox team. They gained a lot of experience and put themselves in position to win in game 7. They are very young and have a solid nucleus on the team. Hopefully they'll be able to take this as a learning experience and improve over the offseason. The Celtics took one on the chin last night. They looked tired out there. After playing with seven guys and pretty much no points from the bench against the Magic, you could see the wear and tare on the starters. We really saw Rondo and Big Baby mature in front of our eyes this year. With KG and Poe back next year, a couple of additions to add to the bench, and the C's will be right back in contention next year. Cav's vs Magic will be a fun series to watch. You'll see two of the most athletic players in the NBA facing off with Lebron and Dwight Howard. Look for Lebron to be Lebron and lead Cleveland to the championship series.

While the stock market continues to rise, the underlying fundamentals of companies, and our economy as a whole, is rotting. Last week we saw a higher than expected initial claims figure and a deeper than expected contraction in retail sales. Both of these indicators show that the consumer is no where near gaining any traction. The more the consumer cuts back, the more their collective psychology changes. The deterioration in the initial claims means that loan defaults (mortgage, credit card, auto, etc) will continue to rise and retail will continue to suffer. This will then put further pressure on the banks. Since many of the "toxic assets" the banks are holding are securitized by some type of loan, this will force them to write down more losses. These losses will be offset by the orchestrated secondary offerings issued by banks. The faux "stress test" results allowed bank share prices to basically double, if not more, in the past two months, to recapitalize to try and cushion themselves from the second wave down which we are approaching.

I'm getting sick and tired of mainstream economists touting a second half recovery in 2009. The nominal figures may show some signs of growth but that will only be temporary due to the massive stimulus packages. Once that wares off, the taxpayers will be left out to dry. The more we go into debt the more we are taking away from standard of living of future generations. These bailouts NEED to stop. This is America, if a company isn't making money then it should fail as the others who came before it. I feel as if the people of this country don't care anymore. If we collectively took some time and reflected on some of the things that are going on around us, a revolution should soon take place. Once the taxpayers realize the government has looted them to bailout the very same people who brought us into this mess, there will be hell to pay. The funny thing, not funny at all actually, is that the media is cheering about the banks repaying TARP money but they don't say a peep about the fact that the insurance companies are now replacing banks as the next in line for the taxpayers money. This has got to end somewhere. When will people wake up? Please prepare yourself by upping your financial literacy and building some rainy day funds because when the realization that we are in a depression right now starts to go mainstream, most people will wish a rainy day was the least of their problems.

Monday, May 11, 2009

Correction phase?

Well it was another great night for Boston sports last night. The Celtics won in an amazing game, Bruins stayed alive in a blowout over the Hurricanes, and the Sox scored a run in the 8th to beat the Rays 4-3. The Celts game was awesome. Big Baby Glen Davis is maturing in front of our eyes folks. Dude is a beast, mind you he is only 6'5'' and is banging with the big boys in the paint. He hit that money 20ft jumper with no time left and did the KG underbite face. Loved every second of it. B's finally played with some energy and smoked the Canes. That cheap shot on Ward at the end of the game was disgusting. The guy basically blindsided him and broke his orbital bone, which may be his eye, but I honestly don't know. Either way, Lucic will go after that guy and tear him apart at one point in game 6, mark my words. Sox continue to just play solid ball. Bay is sneaky unreal. Real quiet, lanky, passive player. Check out the stats and he's looking like the old Manny minus the 72 I.Q. Love his attitude, real humble guy who just rakes up at the plate. Good thing our lineup is stacked because the pitching just hasn't been there yet but it'll come around.

The Fed will most likely expand its Quantitative Easing practices within the next couple of weeks. Yields on the 10-yr have been steadily rising since April 15th. The yields on the 30-yr have been rising since the bad auction last week. Don't forget, the Treasury is still going to attempt to sell $2 trillion more in bonds this year. Think that'll happen?

The judge in the Chrysler bankruptcy decided to not allow the anonymity of the bondholders that are not accepting Chrysler's restructuring offer. They feared for their safety, while trying to get the best deal for their investors. The judge said no, so two of the "non-tarp" lenders, Oppenhiemer and Stairway Capital Management, gave up their rights as a bondholders and more or less conceded saying they will forfeit the money they are owed in order to not be a part of this bankruptcy. To fully present the entire picture to you though, the creditors did have to sign some type of special seal which would keep their names anonymous during the hearings, but as the judge said no. It's not like he did this to be a tough guy, he simply said no to the special seal they were applying for. It's always good to see both sides of the story even if you don't necessarily agree with one side. To me this sounds like things will get messy. Remember the outrage over the AIG bonuses, well that is only the tip of the ice berg.

I didn't get to post on Friday, but I had a couple thoughts lingering in my head from the past week. The dollar is getting annihilated. During the two month rally beginning on March sixth, the dollar is down 7%. I could go over a bunch of reasons why this may be the but the point is, this is a very troubling sign. As I've said before, the dollar is our source of power. The weaker our currency gets, the more purchasing power we lose over our competitors. While it may be nice seeing higher nominal returns on your investments, who really cares if you're being paid back in dollar that are worthless?

The Fed will most likely expand its Quantitative Easing practices within the next couple of weeks. Yields on the 10-yr have been steadily rising since April 15th. The yields on the 30-yr have been rising since the bad auction last week. Don't forget, the Treasury is still going to attempt to sell $2 trillion more in bonds this year. Think that'll happen?

The judge in the Chrysler bankruptcy decided to not allow the anonymity of the bondholders that are not accepting Chrysler's restructuring offer. They feared for their safety, while trying to get the best deal for their investors. The judge said no, so two of the "non-tarp" lenders, Oppenhiemer and Stairway Capital Management, gave up their rights as a bondholders and more or less conceded saying they will forfeit the money they are owed in order to not be a part of this bankruptcy. To fully present the entire picture to you though, the creditors did have to sign some type of special seal which would keep their names anonymous during the hearings, but as the judge said no. It's not like he did this to be a tough guy, he simply said no to the special seal they were applying for. It's always good to see both sides of the story even if you don't necessarily agree with one side. To me this sounds like things will get messy. Remember the outrage over the AIG bonuses, well that is only the tip of the ice berg.

Did today mark the beginning of the dead cat bounce correction? Possibly, but with the government changing the rules everyday you really never know these days. Tons of news flowing out of the market every single day. It's tough to figure out what exactly I should write about.

I'll start off with one of the most startling clips I've seen in some time. I won't go into detail because the video speaks for itself.

Next, we had Meredith Whitney, who has been absolutely spot on with her analysis since the beginning of the crisis, come out and say that the stress test and rally in bank stocks is a complete folly and has been manipulated by the government from the get go. Great way to instill investor confidence wouldn't you say?

I am obviously pessimistic/bearish about the long-term outlook for this economy and country as a whole. While I seem to be an ultra-bear on those fronts, it's important to detach yourself from the big picture and try to trade this market. This is a great traders market if you have some guts and some cash on the sidelines. It is VERY risky out there, but by keeping yourself confined to risk management, capital preservation, and financial staying power, there will be many opportunities for investors.

For the sake of honesty I wanted to share this.

With the benefit of hindsight, I started my short position a week early and paid dearly for it. I got beat up pretty good last week, but continued to add to my short positions to lower my cost basis. Looking back, it was more of an emotional entrance into the shorts rather than a well thought out decision. I am so bearish on the economy, government and market, that sometimes I'll make an emotional decision rather than being rational. While keeping my macro theory in tact, I need to focus on the current market cycle and not the end of the road. It's important to keep track of your investment decisions to better analyze in the future, what catalysts made you either enter or step away from the market at certain points.

Good luck tomorrow and don't forget the popular opinion is rarely the profitable one.

Thursday, May 7, 2009

Crazy week coming to a close

Part two of the how did we get here will be delayed until this weekend. I want to take some time to recap the happenings of this week.

In short...it's crazy out there. We had the results of the "stress test" released today. My thoughts are that this report is the biggest sham so far pulled by this administration's Treasury. The figures they used for "a more adverse" scenario aren't all that adverse for the current environment. Why do you think there was so much "negotiating" between the banks and the Treasury in the time since the tests were finished? Most likely so the Treasury can spin the outcome into some kind of positive. Tiny Tim is grandstanding promoting transparency, which couldn't be further from the truth. Bernanke and the Fed aren't releasing any information as far who got loans, who's participating in some of their programs, and how much money was actually doled out. Pretty sure that creates opaqueness not transparency. All in all, these test results cannot be further from the truth. The banking system may not be completely insolvent, but to say that certain banks need to raise a total of $75 billion is a slap in the face to the American public because these banks will come crawling back to the government for help and will get the capital needed in order to keep the doors open.

We had some very interesting events today. First, consumer credit declined by $11.1 billion and the consensus was for a decline of $4 billion. That's a HUGE decline. With Obama touting that, "credit is the lifeblood of our economy" this figure should make his heart drop. If you haven't realized, consumers are cutting back. They are cutting back on their purchases and their willingness for credit. Combine that with tighter lending standards by banks and we see the seeds planted for a much deeper contraction than what the "adverse scenario" lays out. I look at this as a good sign because it shows that people are deleveraging and hopefully beginning to save. People need to learn to live without the idea that they can take a loan out for anything they want to buy.

There was a bond offering today as well. It didn't go so well. The rate on the 30-yr rose to its highest yield since November. This could be for a number of reasons. It means that investors are demanding a higher return for holding these long term securities. It could signal signs of inflation, signs that foreign countries may no longer want to finance the U.S. spending, or possibly that investors in general are losing confidence in the ability for the U.S. to make good on its debt payments. This auction will most likely get looked over because the bond market moves slow and the media doesn't understand it and therefore cannot cover it. Anyways, what people want to listen to how a bond yield rose by 4 basis points? Not many. You need to watch the bond markets because it absolutely dwarfs the stock market. The traders in the bond market are extremely smart and it's very important to follow their trends.

The stock market was roaring this week. Financials and energy were the leaders of the pack. I think the run up in financials is going to allow the banks that need to raise money to do secondary offerings at much higher stock prices. All these secondary offerings are dilutive to the current shareholders. Each new share issued means that future profits will be spread amongst more people meaning lower EPS which will lower the multiple at which a stock will trade at. That is baked into prices right now but analysts are still overestimating earnings forecasts. We saw a pull back today. Still sitting above the 900 level leaves the market in a tricky position. Most indicators are showing overbought/exhausted conditions. A more telling level will be around 875 which is the critical point of past resistance. If we break through 875 I'd look for the market to be a in pretty heavy downward trend. Tomorrow will be nuts, with the market straddling overbought indicators and the potential for a further run up on "positive" stress test results and what I think will be a lower than expected unemployment rate. I thought the rate would be higher but with ADP figures much lower earlier in the week, that will most likely lead to the unemployment rate temporarily easing.

This puts investors in a very precarious position. The fundamentals are still deteriorating which means stock prices should be lower. Technicals show that the market is overbought which means that it should be lower. All the bad news that has been dumped on us the past few weeks signals the market should be lower, but there is no should in stock markets. Using a quote from the legendary Bill Belechick, the market "is what it is". Usually when things look as if they should be one way, the market will do the opposite. While the market looks as if we'll see a selloff heading into the weekend, a key indicator to watch is the dollar (DXY). It's resting on a resistance level that if pushed lower, CAN but not necessarily WILL, push the market higher. If the dollar loses value, assets priced in dollars will go up. It's sort of like a seesaw. So while the market feels like it should go lower in the next few sessions, please be aware that because something should happen, i'd be willing to bet that it won't. The popular opinion is rarely the profitable one.

Look for an interesting session tomorrow heading into the weekend. Good luck!

Tuesday, May 5, 2009

How did we get here?

Sorry the posts have been a bit inconsistent. I am still trying to figure out the best way to communicate my thoughts/ideas in a well laid out format.

Today I will give an overview as to how we got into the position we are in today. I will elaborate on this in the next few days to give you a more detailed summary to show how embedded this problem has become in our daily lives.

First off I'd like to start off with a few Boston sports tidbits.

-Celtics had an unbelievable comeback in game 1 on Monday. Plain and simple - they didn't deserve to win. Rondo played the sloppiest game I've seen in while, Ray couldn't hit a shot, we had a ton of careless turnovers and looked very tired overall. With that said, I still believe the Celts will win this series.

-Bruins played with no energy in game 2. You cannot win a playoff hockey game by just showing up. Still think the B's win in 5.

-Sox are beat the Yanks last night. That should make us all happy, but their pitching is worrying me. Absolutely love the lineup though. Ortiz needs to start hitting or I want a mega deal for Miguel Cabrera by the all-star break. Honestly, we have playoff basketball and hockey right now, so I haven't followed the Sox as faithfully as I should. Can't knock that.

I can only imagine what some people's take is on the financial crisis. It's scary food for thought. Some people have the wrong idea as to how we got here, some people have a few correct thoughts as to how we got here and some people simply don't care. I for one, care deeply because this situation effects my life, my family and friends, and will no doubt have a major effect on the future generations of this country.

This will be the first of a series of posts which detail how we got here.

Causes of the current financial crisis can be traced back as far as twenty years or so. Imbalances in the banking sector have been growing since the mid to late eighties. Fast forward to 1998 when the Federal Reserve bailed out Long Term Capital Management. This was when the idea of "too big to fail" was born. Then Fed chairman, Allan Greenspan, believed LTCM posed serious systemic risk to the financial markets and therefore must be bailed out to avoid a collapse. Irony runs deep in this issue and in the financial markets as a whole. LTCM was run by a man named John Meriweather, for those who have read Liar's Poker may remember, was the head of bond trading at Saloman Brother's in the 1980's. Saloman Brother's pioneered the trading of mortgage backed securities, otherwise known as "toxic assets" which are a major reason our banks are insolvent today, which we will get to later. This bailout was the first seed to be planted into the psychology of investors and CEO's across the country. If a company got so big that it was important to the "system", than if shit hits the fan, it'll get bailed out.

Next we had the dot.com boom of the late 1990's. This was when companies that had no way creating revenue/earnings went public and their stock prices went soaring through the roof. It made absolutely no sense, but the prevailing bias of market participants was that because they were a dot.com stock, they had unlimited earnings power in this new age of the internet and technological advancement. We saw the NASDAQ (see chart below) rise from 1500 in mid 1997 to 5000 in March of 2000.

This created bubbles within the capital markets and would later trickle down into the economy. Lots of new wealth was created in this short time. Most of it was caused by the rise of financial assets, which is not backed by anything tangible. Many people did not know how to handle this new found wealth. They went out and bought multiple houses, cars, luxury items (jewelry, clothing, vacations, airplanes, boats, you get the picture), which only exacerbated our problem of having capital misallocated. The longer capital is wrongfully invested, the larger a bubble will grow.

Think about giving a kid money while his/her parents are away. If the kid has $10 a day to spend on food, the money will mostly be used on pizza or candy. Now since the pizza and candy companies are making more money, they will produce more. Since the kid doesn't want fruit and vegetables, the apple and the carrot companies have less profits and therefore produce less. This isn't healthy for the industry as a whole because they all count on one another for healthy and sustainable growth. So as you can see, allowing someone with new found wealth to spend freely, will create imbalances which lead to bigger problems.

Once the dot.com bubble popped in 2000, markets were sent crashing down and recession was imminent. Recession is actually a good thing, contrary to popular opinion. It means that businesses were growing too fast for their own good and need time for a healthy pause to almost re-balance themselves. Recessions allow the poorly allocated capital to be reallocated to productive businesses which foster economic growth. Think energy, infrastructure, utilities, semi-conductors, things that will improve our daily life and allow both people and businesses to become more efficient. A tool that can used to make investors allocate capital more productively is interest rates. An interest rate is simply the cost of money. If you have a $100 loan with a 1% interest rate, you owe the lender $1 for each interest payment. If you have a $100 loan with a 10% interest rate, you now owe the lender $10 each interest payment and must therefore invest your money wisely in order to come up with enough to cover your interest payments.

In 2000 Allan Greenspan clearly did not want the U.S. to enter recession. As I said before recession is good because the private market will reallocate capital to more productive businesses. In order to avoid recession, Greenspan lowered interest rates, with the benefit of hindsight, was one of the worst possible moves he could have made.

Here is a chart of the Federal Funds Rate from 2000-2006.

As you can see rates were cut in half in the following year and half and eventually stayed below 2% from late 2001 all the way until early 2005. Now some of you may ask why is lowering interest rates such a bad idea. Well when we had a giant bubble build up in the stock market which led to the misallocation of trillions of dollars, why would we further exacerbate the problem of misallocation by making money cheaper to borrow? Makes no sense to me.

This created the world's largest credit bubble. The credit bubble acted like a cancer, spawning new bubbles in other sectors. The most dangerous bubble, which I will write about next, was real estate. Rather than investing in stocks, which may cost anywhere from $1/share to $500/share, overnight millionaire investors could now speculate in the biggest market in the U.S. Why flip stocks when you can flip houses? Why flip houses when you can flip mansions? Tomorrow I'll go into the boom and bust of the real estate market in the U.S. and show you how that factored into this financial mess.

Sunday, May 3, 2009

Random rambling

I'll keep it quick and concise this morning. Just had a few random thoughts I wanted to throw out there.

-Celtics won game 7. It was the best team effort they have put together all post season. Eddie House awoke from the dead, Scal was unreal banging those 3's, Mikey Moore, who looks eerily similar to the creature, the Predator, had a couple momentum baskets, and even Marbury looked a bit more confident in his shot and driving to the basket. Overall great effort by the C's and I like their match-ups against Orlando. Let Howard have his points and make the rest of the team win those games. C's are going to be tired, but at this point of the season, they are playing on emotion/adrenaline.

-Bruins looked great in their opener on Friday. They didn't come out flat, like all the "analysts" predicted they would. The B's pounded Carolina in the regular season. Look for this series to be wrapped up in 5.

-Sox finally beat the Ray's. They play us tough. I hate the stadium in Tampa Bay....can never get excited watching games played there. Looks dark, gloomy, quiet and is a turf field. Exciting time to be a Boston sports fan. I feel like I've been telling myself this for about four years now. We just have top echelon teams in every league. While, this won't last forever, take a second to reflect on our recent success. It's unreal and I love it.

-Stress test results were supposed to be released tomorrow, but have been delayed until Thursday. This notion of the stress test being a well conducted analysis of the banks is foolish. This will buy the government a few more days to prep their PR lemmings to slant these results into some kind of positive, which couldn't be further from the truth.

-The market is up almost 30% from the March 6 lows. The finance sector is up 71% in that time frame. I started to build a short position in the finance sector via ETF on Friday.

-We have unemployment figures coming out this week. Look for unemployment to jump to 9%. If we used the pre-Clinton unemployment calculation, we'd be around 16%. Jobs are still being shed. The thing to watch for is, where are jobs being lost. We have begin to see job losses increase in small businesses. This is something you want to keep on your radar, because this is the biggest sector for American employment and when we see deterioration there, it should be worrisome.

-When is the government going to realize that the consumers are tapped out. Credit it not the lifeblood of our economy. Think about it, credit is another word for debt. We have a President, who tells us banks need to lend again because "credit is the lifeblood of our economy". Substitute the word debt for credit and you'll realize how idiotic that logic is. "Debt is the lifeblood of our economy." Ehhh I don't know if I can agree with you there Pres. I think it's time to allocate our resources in more productive manner, so that our entire economy isn't finance and consumer based. If anything goes wrong with our financial experiments, or if consumers retrench, our whole mirage of wealth seemingly evaporates. Doesn't sound healthy to me.

-Anyone see Tiger Woods' 4-iron approach shot on the 15th hole yesterday? The guy is unbelievable.

-Did you read the Sage of Omaha's comments on the real estate? Doesn't paint too bright of an outlook for the Pollyanna's.

-Ricky Hatton is a leather faced punching bag. Someone tell his corner to throw in the towel.

Heading out to play golf in Lakeville.

Friday, May 1, 2009

Period of uncertainty

Due to the Celtics game 6 and Sam Adams summer ale, yesterday's post had to be delayed until this morning. A few comments on the game: The Celtics looked tired at the end of the game; Not having a defensive presence is killing them in the paint; With Ray Allen on fire, why is Pierce jacking up that elbow jumper in OT? I love Pierce and think he is one of the best pure scorers in the league, but he just banged 3 HUGE shots in OT in game 5. Share some love with Ray and let him hit that game winner dude. The Celts will win the series at home tomorrow, but think about the wear and tear on those dudes legs. Rondo, Ray, Pierce and now even Big Baby are all playing 50+ minutes a game and are going to tire out come next series. Not having KG is akin to the Patriots missing Brady. It's a sad thing to watch such a talented team struggle because they are missing a main piece to the puzzle. Enough sports talk or else I'll rant all day.

I speculated that the Fed was going to announce further quantitative easing on Wednesday and was incorrect. The dollar clawed back after their non-announcement, interest rates rose on the 10-yr, and the short 7-10 yr Treasury ETF saw gains. Caught off guard by the non-announcement, I thought about it for a while and it made more sense. Everyone thought the Fed was going to buy more debt. They acted like contrarians and didn't. Last time the Fed announced they were going to buy Treasuries, rates still rose. The Fed doesn't want monetize the debt if rates are going to keep rising in the face of them buying. The announcement said, "The committee will continue to evaluate the timing and overall purchases of securities in light of the evolving economic outlook and conditions of the market." There is no doubt they will have to buy more because the housing recovery plans assume mortgage rates will be low and with the bond traders pushing rates up, this would create a problem. This was a smart move by the Fed because they are going to keep traders on their toes and will leave any investors shorting the bonds at risk. At the same time this creates more uncertainty surrounding the market because at anytime the Fed can announce more debt purchases. Overall this is negative for the dollar, which I believe, is the main barometer of economic health. The weaker our dollar gets, the more purchasing power we lose, the more our standard of living goes down. The current administration doesn't seem to care much about the dollar, but that's an entirely different debate.

Yesterday, Chrysler announced they are going to claim bankruptcy. If I was a creditor of the company, I would have balked at Chrysler's offer. They would basically get pennies on dollar for the money they are owed. I would take my chances in bankruptcy, hoping to get more than what Chrysler was offering. This is going to be an interesting event to follow. Going into bankruptcy is obviously not a good thing. The government wants this to be a quick 30-90 day process. This is going to be a long drawn out process unless someone from the government strong arms some "friends" in bankruptcy court. This could be an example for what's to come with other companies that could potentially go into bankruptcy. Investor psychology will be effected by this and will be important to track. Real tough trying to discount the bankrupcty case into stock prices.

Goldman had a $2 billion dollar debt offering and raised $750 million in a stock offering. If the company that runs the world is building it's capital base, what does that tell you? The "too big to fail" banks are in need of capital says the make believe stress test regulators. Did we really need to test these banks to know they are under tremendous stress? C'mon that's ridiculous. Look at what's been going on in these companies since October 2007 and you'll see if they are stressed. This test is just another way for the government to buy time before the day of reckoning. Banks are now arguing that the test doesn't show conclusive evidence they need to raise capital. The "too big to fail" banks are insolvent and do not need capital. They need to fail. Stop all this propping up and creation of zombie banks which will ultimately be ran by the government. My take is that these tests will be used as a backdoor way to nationalize the big banks. Sneaky, but a lot better than just announcing outright nationalization of the banks....well atleast from a PR prospective. These damn Keynesians are ruining our once robust economy.

I feel like this market is running out of gas. April was the first month of the new quarter and investors will like the way it started. The sell in May and go away mantra is starting to surface. Investors have been shrugging off horrendous news for quite some time now. The SP is hitting resistance around 900, which will be tough to break through. While this 23% run up since the May 6 low of 666, could have more legs, I think it's an opportune time to look to build some short positions. Many people are claiming this new bull market will continue but remember the popular opinion is rarely the profitable one.

That's it for now. Be back after the market closes. Have a good day.

I speculated that the Fed was going to announce further quantitative easing on Wednesday and was incorrect. The dollar clawed back after their non-announcement, interest rates rose on the 10-yr, and the short 7-10 yr Treasury ETF saw gains. Caught off guard by the non-announcement, I thought about it for a while and it made more sense. Everyone thought the Fed was going to buy more debt. They acted like contrarians and didn't. Last time the Fed announced they were going to buy Treasuries, rates still rose. The Fed doesn't want monetize the debt if rates are going to keep rising in the face of them buying. The announcement said, "The committee will continue to evaluate the timing and overall purchases of securities in light of the evolving economic outlook and conditions of the market." There is no doubt they will have to buy more because the housing recovery plans assume mortgage rates will be low and with the bond traders pushing rates up, this would create a problem. This was a smart move by the Fed because they are going to keep traders on their toes and will leave any investors shorting the bonds at risk. At the same time this creates more uncertainty surrounding the market because at anytime the Fed can announce more debt purchases. Overall this is negative for the dollar, which I believe, is the main barometer of economic health. The weaker our dollar gets, the more purchasing power we lose, the more our standard of living goes down. The current administration doesn't seem to care much about the dollar, but that's an entirely different debate.

Yesterday, Chrysler announced they are going to claim bankruptcy. If I was a creditor of the company, I would have balked at Chrysler's offer. They would basically get pennies on dollar for the money they are owed. I would take my chances in bankruptcy, hoping to get more than what Chrysler was offering. This is going to be an interesting event to follow. Going into bankruptcy is obviously not a good thing. The government wants this to be a quick 30-90 day process. This is going to be a long drawn out process unless someone from the government strong arms some "friends" in bankruptcy court. This could be an example for what's to come with other companies that could potentially go into bankruptcy. Investor psychology will be effected by this and will be important to track. Real tough trying to discount the bankrupcty case into stock prices.

Goldman had a $2 billion dollar debt offering and raised $750 million in a stock offering. If the company that runs the world is building it's capital base, what does that tell you? The "too big to fail" banks are in need of capital says the make believe stress test regulators. Did we really need to test these banks to know they are under tremendous stress? C'mon that's ridiculous. Look at what's been going on in these companies since October 2007 and you'll see if they are stressed. This test is just another way for the government to buy time before the day of reckoning. Banks are now arguing that the test doesn't show conclusive evidence they need to raise capital. The "too big to fail" banks are insolvent and do not need capital. They need to fail. Stop all this propping up and creation of zombie banks which will ultimately be ran by the government. My take is that these tests will be used as a backdoor way to nationalize the big banks. Sneaky, but a lot better than just announcing outright nationalization of the banks....well atleast from a PR prospective. These damn Keynesians are ruining our once robust economy.

I feel like this market is running out of gas. April was the first month of the new quarter and investors will like the way it started. The sell in May and go away mantra is starting to surface. Investors have been shrugging off horrendous news for quite some time now. The SP is hitting resistance around 900, which will be tough to break through. While this 23% run up since the May 6 low of 666, could have more legs, I think it's an opportune time to look to build some short positions. Many people are claiming this new bull market will continue but remember the popular opinion is rarely the profitable one.

That's it for now. Be back after the market closes. Have a good day.

Subscribe to:

Comments (Atom)